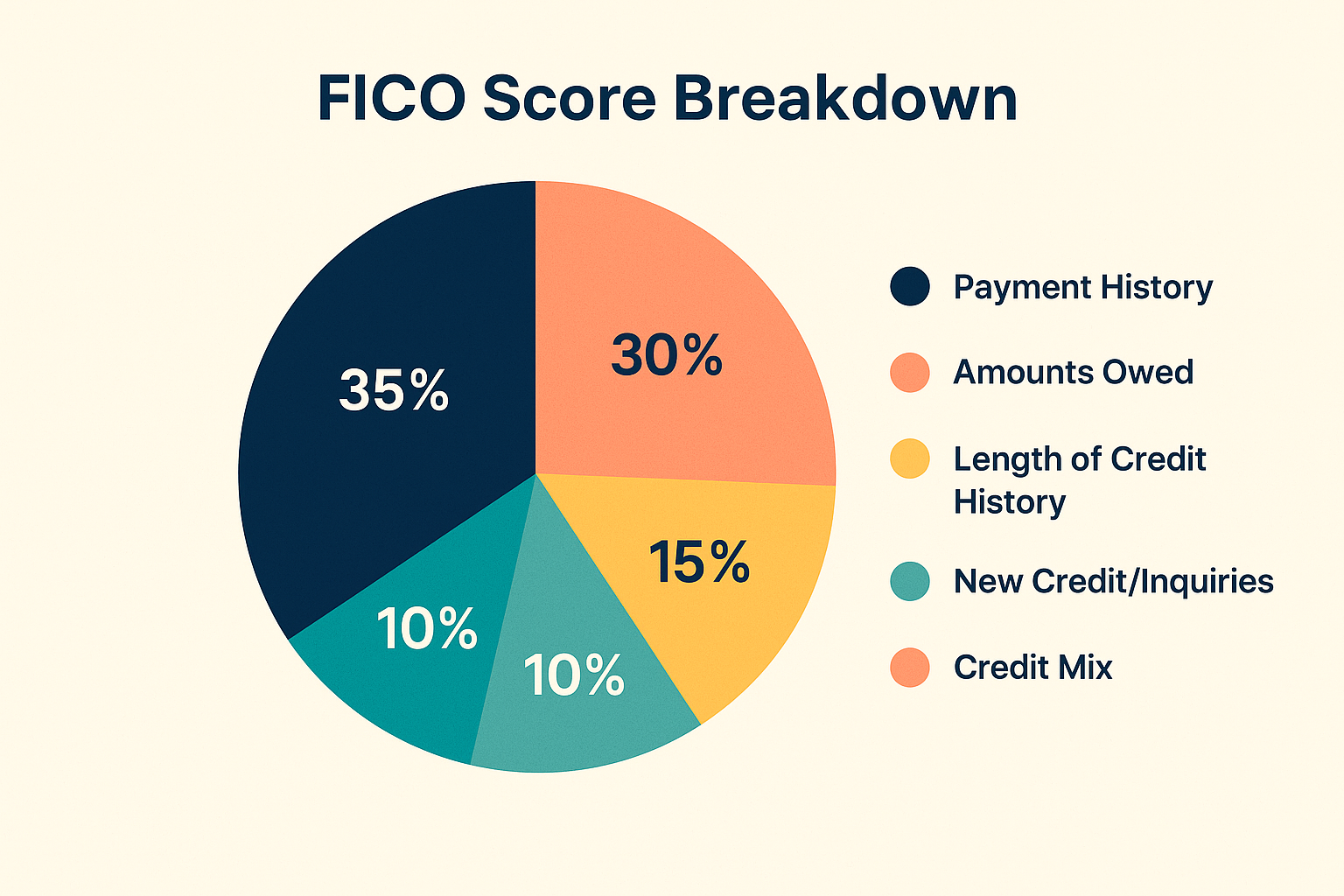

This guide breaks down the FICO formula. Understanding these five areas is the foundational key to any serious, successful credit repair attempt.

A credit score is a three-digit number, typically ranging from 300 to 850, that summarizes how risky you look to lenders based on your past and current borrowing behavior. It is designed to predict how likely you are to pay back debts on time.

The **“FICO score”** is the most widely used brand, created by the Fair Isaac Corporation. While various models exist (like VantageScore), FICO is the standard most major lenders rely on when deciding whether to approve you and what terms to offer.

If you want to know why your score is low or how to fix it, these are the five critical areas to focus on.

This is the most important factor. It answers a simple question: Do you pay your bills on time? This includes credit cards, mortgages, student loans, and car loans.

This measures how much of your available credit you are using. This is called your **credit utilization ratio** (Total Balances ÷ Total Limits).

FICO looks at the age of your oldest account, your newest account, and the average age of all your accounts. Longer history shows more experience and responsibility.

This reflects how often you apply for new credit. Each application results in a **“hard inquiry”** that can slightly lower your score for a short time.

FICO likes to see that you can handle different types of credit: **revolving credit** (like credit cards) and **installment credit** (like mortgages or auto loans).

Understanding the FICO formula is only half the battle. Your next step is to find out your current score and pull your reports to identify the exact items holding you back.

Don't wait for errors to disappear. Get the **Ultimate Dispute Letter Kit** to start challenging items immediately after finding them in your report.

Download FREE Dispute Templates